The Best Strategy To Use For Home Renovation Loan

The Best Strategy To Use For Home Renovation Loan

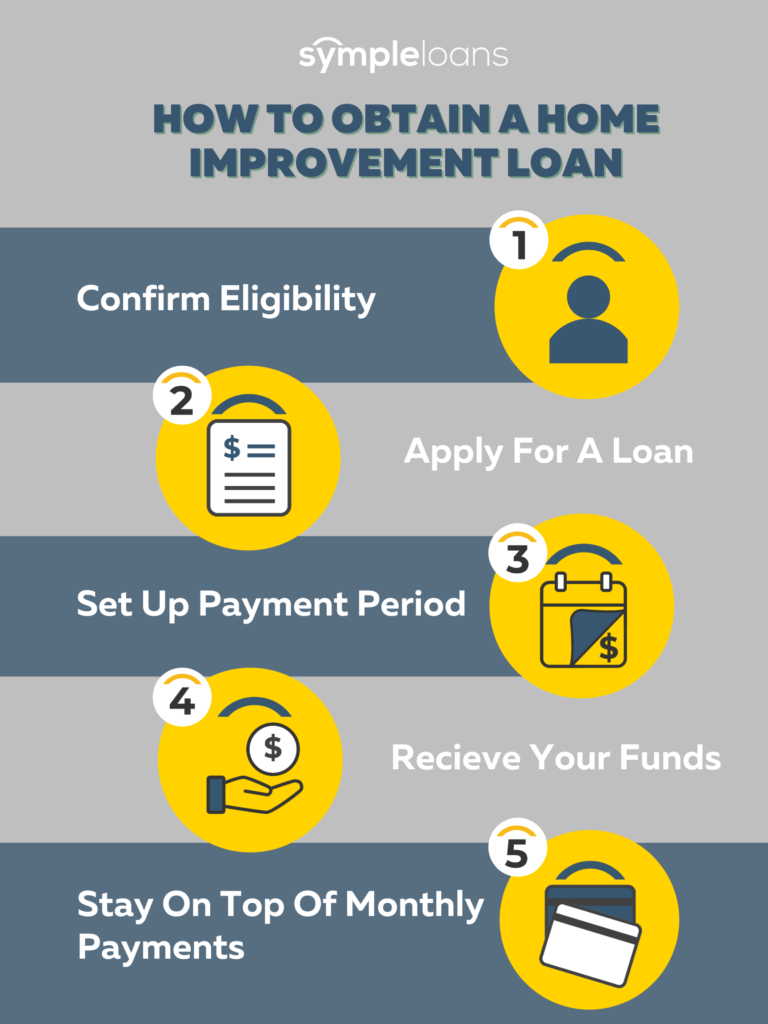

Blog Article

Rumored Buzz on Home Renovation Loan

Table of ContentsSee This Report about Home Renovation LoanHome Renovation Loan Things To Know Before You Get ThisThe Main Principles Of Home Renovation Loan The Of Home Renovation LoanLittle Known Questions About Home Renovation Loan.The Ultimate Guide To Home Renovation Loan

Possibly. In Canada, there go to least a number of different ways to add renovation costs to home loans. In some cases lenders refinance a home to gain access to equity needed to complete small remodellings. If your current home mortgage balance is below 80% of the current market value of your home, and your household revenue supports a bigger home mortgage quantity, you might certify to re-finance your home loan with extra funds.This allows you to finish the job required on the home with your own funds. When the restorations are complete, the lending institution launches funds to you and your mortgage quantity boosts. You might acquire a home with a home loan of $600,000, and an improvement amount of $25,000 (home renovation loan).

A home enhancement loan can provide quick funding and adaptable repayment alternatives to home owners. Home renovation loans may come with greater prices and charges for customers with negative credit report. These financings can help construct your credit score and increase the worth of your home, yet they likewise have potential drawbacks such as high fees and secured options that put your properties at threat.

Unknown Facts About Home Renovation Loan

You might money everything from little improvements to cellar conversions. Individual loans are one common kind of home renovation funding, yet other kinds like home equity lendings and cash-out refinancing supply their very own rewards. Like all financings, home enhancement lendings have downsides. As an example, if you do not have stellar credit score, it's likely that you'll be supplied high rate of interest and fees if accepted.

Home improvement lendings aren't for every person. Elements like charges, high rates and hard credit history pulls can detract from the lending's worth to you and cause economic tension down the roadway. Not every loan provider bills the same costs. Your lending may have an origination charge subtracted from the complete amount you obtain or contributed to the quantity you obtain.

Little Known Questions About Home Renovation Loan.

Both can be prevented. The higher your passion price, the more you will certainly have to spend each month to fund your home jobs.

Nevertheless, some lendings are safeguarded either by your home's equity or by another property, like a cost savings or investment account. If you're not able to pay your lending and get in default, the lender could seize your security to please your financial debt. Even if a safeguarded funding comes with reduced prices, the threat possibility is a lot higher and that's a crucial variable to think about.

Raising your debt use by utilizing a HELOC or credit score card can also lower your helpful site credit rating. And if you miss out on any type of payments or default on your lending, your loan provider is most likely to report this to the credit score bureaus. Missed out on payments can remain on your credit scores record for up to seven years and the better your credit score was previously, the more it will certainly drop.

Unprotected home improvement lendings generally have fast financing rates, which could make them a much better financing option than some options. If you need to obtain a lump amount of cash to cover read this a project, an individual financing may be a good idea. For ongoing jobs, take into consideration a charge card, line of credit rating or HELOC.

How Home Renovation Loan can Save You Time, Stress, and Money.

Concerning 12.2. They use some rewards in exchange - home renovation loan. Financing times are quicker, because the lending institution does not have to examine your home's value which also means no closing costs.

You put up your home as collateral, driving the rate of interest rate down. This also might make a home equity funding much easier to qualify for if you have inadequate credit.

Existing ordinary rate of interest: Concerning 9%. A HELOC is a protected loan and a revolving credit line, suggesting you attract money as required. Rates of interest are frequently reduced but generally variable, so they change with the market. As with home equity lendings, the largest downsides are that you could shed your home if you can not pay what you owe and that shutting expenses can be costly.

, you would take out a new mortgage for more than you owe on your residence and make use of the distinction to fund your home enhancement task. Shutting expenses can be high, and it might not make sense if passion rates are greater than what you're paying on your existing mortgage finance.

What Does Home Renovation Loan Do?

The optimum quantity is $25,000 for a single-family home, reduced than most of your various other choices. You may require to provide collateral depending on your financing amount (home renovation loan).

Externally, getting a new bank card might not seem like an excellent idea for moneying home renovations due to their high passion prices. Yet if you have check my site great credit score, you may get approved for a card that supplies a 0 percent introductory APR for a marketing duration. These durations typically last between 12 and 18 months.

That makes this method best for short- and medium-term tasks where you have a great price quote of your costs. Meticulously take into consideration the potential impact that tackling more debt will have on your economic health. Even before comparing lending institutions and exploring the information, perform a monetary audit to guarantee you can manage even more financial debt.

And don't forget that if you cash out investments that have actually risen in value, the money will certainly be strained as a capital gain for the year of the withdrawal. Which implies you might owe cash when you submit your tax obligations. If you will acquire a fixer top, you can include the quantity you'll require to fund the restorations into your home mortgage.

Unknown Facts About Home Renovation Loan

Report this page